The IRS previously used the Consumer Price Index (CPI) as a measure of inflation prior to 2018. However, with the Tax Cuts and Jobs Act of 2017 (TCJA), the IRS now uses the Chained Consumer Price Index (C-CPI) to adjust income thresholds, deduction amounts, and credit values accordingly.

The new inflation adjustments are for tax year 2024, for which taxpayers will file tax returns in early 2025. Note that the Tax Foundation is a 501(c)(3) educational nonprofit and cannot answer specific questions about your tax situation or assist in the tax filing process.

In 2024, the income limits for all tax brackets and all filers will be adjusted for inflation and will be as follows (Table 1). The federal income tax has seven tax rates in 2024: 10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent, and 37 percent. The top marginal income tax rate of 37 percent will hit taxpayers with taxable income above $609,350 for single filers and above $731,200 for married couples filing jointly.

The alternative minimum tax (AMT) was created in the 1960s to prevent high-income taxpayers from avoiding the individual income tax. This parallel income tax system requires high-income taxpayers to calculate their tax bill twice: once under the ordinary income tax system and again under the AMT. The taxpayer then needs to pay the higher of the two.

The AMT uses an alternative definition of taxable income called alternative minimum taxable income (AMTI). To prevent low- and middle-income taxpayers from being subject to the AMT, taxpayers are allowed to exempt a significant amount of their income from AMTI. However, the exemption phases out for high-income taxpayers. The AMT is levied at two rates: 26 percent and 28 percent.

The AMT exemption amount for 2024 is $85,700 for singles and $133,300 for married couples filing jointly (Table 3).

In 2024, the 28 percent AMT rate applies to excess AMTI of $232,600 for all taxpayers ($116,300 for married couples filing separate returns).

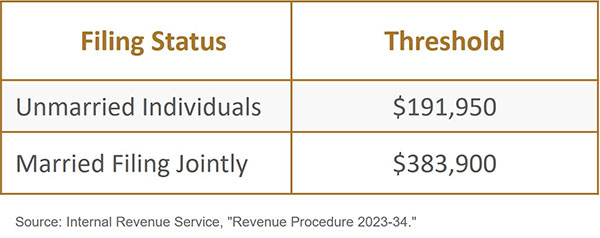

AMT exemptions phase out at 25 cents per dollar earned once AMTI reaches $609,350 for single filers and $1,218,700 for married taxpayers filing jointly (Table 4).

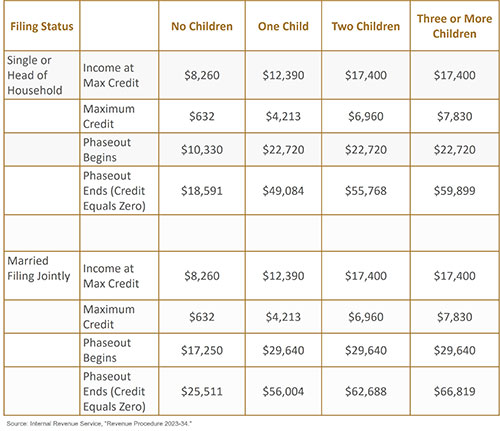

The maximum child tax credit is $2,000 per qualifying child and is not adjusted for inflation. The refundable portion of the child tax credit is adjusted for inflation and will increase from $1,600 to $1,700 for 2024.

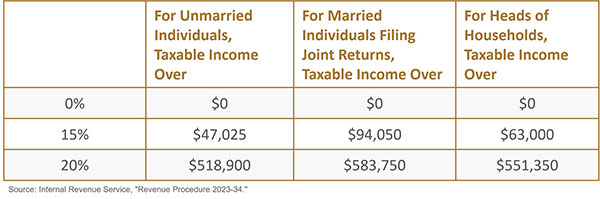

Long-term capital gains face different brackets and rates than ordinary income (Table 6.)